Pagaya Technologies Ltd. (NASDAQ: PGY)

AI-Driven Credit Infrastructure Under Stress: Growth, Volatility, and Sustainability

Company Overview & Investment Snapshot

Pagaya Technologies Ltd. is an AI-driven credit infrastructure company focused on expanding access to consumer lending by reassessing borrowers rejected by traditional banks. Founded in 2016 and headquartered in New York, the company partners with fintechs and financial institutions to originate loans and distribute them to institutional investors via securitizations and related structures, largely avoiding balance-sheet credit risk.

While Pagaya has delivered strong revenue growth, record securitization activity, and a recent return to GAAP profitability, its risk profile remains elevated. Large historical losses, extreme share-price volatility, insider selling, and sensitivity to credit and capital-market cycles continue to weigh on investor confidence.

After a sharp correction from peak levels, the stock trades at forward valuations that appear reasonable but remain highly execution dependent.

Recent Developments & Operating Momentum

Pagaya posted a solid Q3 2025, reporting record revenue of $350.17 million and net income of $22.55 million, reflecting meaningful improvement after years of losses. Management raised full-year guidance, projecting network volume of up to $10.75 billion. This progress follows FY2024, when revenue rose 27% to $1billion plus but net losses widened to $401 million, highlighting profitability concerns.

Capital markets activity remained strong, with a $500 million consumer-loan ABS transaction in December 2025, its eighth of the year—bringing 2025 capital commitments above $8 billion and total ABS issuance to $7.6 billion. Liquidity was further supported by expansion of the revolving credit facility to $132 million at lower cost and issuance of $500 million senior unsecured notes at 8.875% due 2030, improving near-term flexibility while increasing leverage.

Growth Outlook & Market Expectations

Street estimates project revenue of approximately $1.8 billion by 2028, implying a CAGR of about 17%, with potential net income of roughly $312 million assuming operating leverage and stable credit performance. Pagaya reported GAAP net income of $17 million in Q2 2025 and followed with another profitable quarter, suggesting a possible inflection point. Management guides to FY2025 GAAP net income of $55–$75 million.

Analyst sentiment remains constructive, with a consensus “Strong Buy” rating and average 12-month price targets in the $37–$40 range, spanning from approx $27 on the low end to $54 on the high.

Key Risks & Structural Concerns

Notwithstanding recent improvements, Pagaya faces material risks. Net losses of $401 million in 2024 raise concerns over cost discipline and the durability of profitability. The stock remains highly volatile, trading roughly 45–50% below recent highs, while insider selling over the past three months totalled 97,425 shares across nine transactions.

The business is also exposed to partner concentration and subprime credit risk, where any pullback in partner activity or economic downturn could materially impact volumes and performance. In addition, evolving regulation of AI-based underwriting and competition may pressure margins and growth.

Valuation & Price Targets

As of December 2025, Pagaya trades in the $22–$24 range, implying a market capitalization of approximately $2 billion and a 52-week range of $8–$45. While valuation metrics appear modest relative to high-growth fintech peers, they assume sustained profitability and benign credit conditions.

Medium-term (12–18 months): Upside potential of ~25–40% under stable credit conditions, with downside risk to $18–$20 if execution or credit trends weaken.

Long-term (3–5 years): A valuation of $35–$45 is achievable, if demonstrates sustained GAAP profitability, scales revenue, and reduces partner and credit-cycle risks.

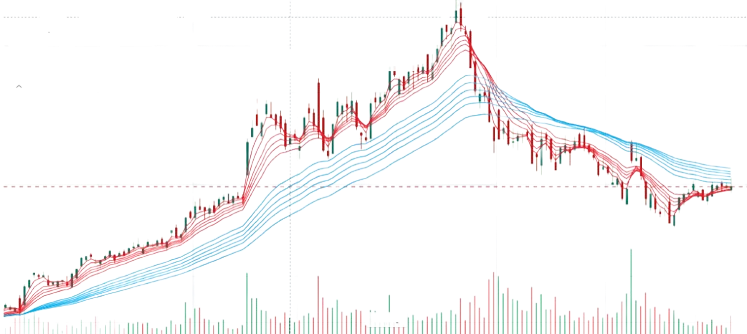

Technical view and Chart positioning

The stock has moved from a strong uptrend into a healthy correction and is now showing signs of stabilization. Technically, selling pressure has eased, volatility has reduced, and short-term averages are flattening, indicating early base formation rather than continued weakness. From an investment perspective, downside risk appears to be moderating, but a clear upside trend will only be confirmed if the price sustains above ₹31–32 with volume. The setup favors cautious accumulation or watchlist positioning rather than aggressive buying.

Investment View & Conclusion

Pagaya represents a high-risk, high-reward exposure to AI-enabled consumer credit infrastructure. Recent operational progress and profitability are encouraging, but they remain overshadowed by historical losses, volatility, insider selling, and exposure to subprime credit cycles. The roughly 50% correction from recent highs suggests growing market skepticism.

View: Suitable for investors with high risk tolerance. Existing shareholders may consider holding with disciplined risk management, while new investors should await and accumulate either lower entry levels or clearer evidence of sustainable profitability across economic cycles.

Disclaimer

This research is intended solely for educational purposes and should not be interpreted as investment advice. Readers are encouraged to conduct their own due diligence and/or consult a licensed financial advisor before making any investment decisions. All information and data presented are sourced from publicly available company filings, analyst reports, and third-party sources believed to be reliable. While this report has been prepared independently, the views expressed are personal and may contain errors or subjective bias. The author holds no financial or personal interest in the company discussed and does not own any position at the time of writing.