Power Solutions International (NASDAQ: PSIX): Growth Ignites, Conviction Tested

Data-Center Tailwinds Push Technical Upside While Credibility Risks Shape the Trade

Power Solutions International (PSIX) occupies a rare position at the intersection of exceptional revenue momentum and persistent investor skepticism. The company has emerged as a meaningful beneficiary of the AI-led data-center infrastructure cycle, delivering record revenues and triple-digit earnings growth in FY2025.

Despite this performance, PSIX trades at approximately 12.4x trailing earnings, a steep discount to industrial and growth peers. This valuation gap reflects sustained concerns around earnings quality, governance credibility, and disclosure risk. While upside potential remains meaningful if these concerns abate, the burden of proof has firmly shifted to management.

Company Overview

Power Solutions International, Inc. designs, engineers, manufactures, and markets emission-certified engines and integrated power systems for global markets. Headquartered in Wood Dale, Illinois, the company operates across North America, Europe, Asia-Pacific, and other international regions.

As a subsidiary of Weichai America Corp., PSIX offers:

Packaged power systems and generator sets

Compression-ignition and spark-ignition engines

Power solutions for data centers, oil & gas, industrial equipment, and transportation

The company employs approximately 700 people and has strategically repositioned itself toward high-growth data-center and AI-infrastructure demand, now its primary growth driver.

Recent Financial Performance

Q3 FY2025: Record Results

PSIX delivered materially stronger-than-expected Q3 FY2025 results:

Revenue: USD 203.8 million (+62% YoY; vs. USD 169.2m estimated)

Net Income: USD 27.6 million (+59% YoY)

Nine-month FY2025 performance:

Net Sales: USD 531.2 million (+60% YoY)

Net Income: USD 97.9 million (+113% YoY)

Growth was primarily driven by an USD 85.3 million year-over-year increase in power-systems revenue, largely attributable to hyperscale and AI-related data-center demand.

Strategic Developments

August 2025: Secured a USD 135 million committed credit facility, extending maturities to July 2027 and strengthening liquidity

August 2025: Entered a strategic cooperation agreement with HD Hyundai Infracore to expand industrial engine offerings

September 2025: Appointed Zhaoying (Dorothy) Du as General Counsel and Corporate Secretary

October 2025: Board restructuring with increased Weichai-affiliated director representation

These actions signal an effort to reinforce operational capacity and governance structure amid accelerated growth.

Margin Compression & Earnings Quality

Despite record top-line performance, profitability indicators have weakened:

Gross margin: Declined from ~29% to ~23% (≈500 bps contraction)

Operating cash flow: Underperformed relative to reported net income

Accounts receivable: Growing faster than revenues, raising working-capital concerns

Management attributes margin pressure to product-mix shifts toward lower-margin data-center solutions and temporary inefficiencies during rapid capacity expansion. However, the persistence of these trends continues to weigh on investor confidence.

Major Risk Factors

1. Securities Law Investigations

Multiple law firms-initiated investigations during November–December 2025, focusing on guidance consistency, disclosure adequacy, and earnings transparency.

2. Historical Accounting Overhang

The company’s former CEO was charged with accounting fraud in 2019, leading to SEC settlements in 2020. Although related to prior management, this history amplifies sensitivity to current disclosure issues.

3. Competitive Landscape

PSIX competes against industry leaders such as Cummins, Caterpillar, and Generac, all of which possess superior scale, customer relationships, and pricing power.

4. Customer Concentration

Heavy exposure to the data-center segment increases vulnerability to hyperscaler capex cycles and potential demand normalization.

Investment Thesis

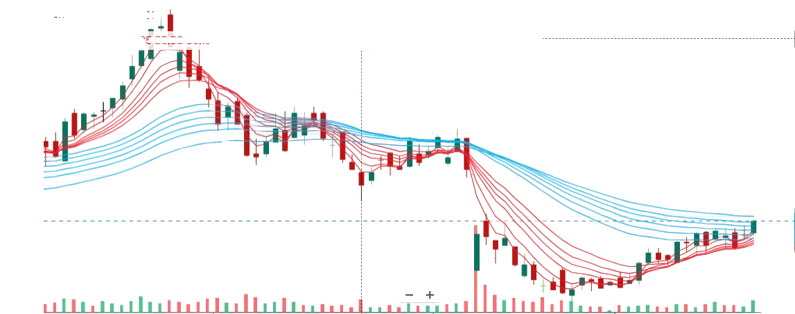

PSIX is currently consolidating near USD 68.73, following a decisive recovery from recent lows, with early indications of renewed bullish momentum. From a technical standpoint, the stock continues to display constructive trend-reversal characteristics, though its wide 52-week trading range underscores elevated volatility. Sustained price action above key cloud and trend support levels remains critical to preserving a bullish bias.

Outlook

Short Term (1–3 months):

Positively biased, with momentum favoring further upside as long as the stock holds above USD 60, supported by improving technical structure and consolidation strength.Medium Term (3–9 months):

Constructively bullish, contingent on confirmation of earnings durability, margin stabilization, and improved cash-flow visibility. Successful fundamental validation could support a continuation of the recovery trend.Long Term (9–24 months):

Bullish with selective conviction, driven by sustained AI and data-center infrastructure demand, provided governance credibility strengthens and operational execution remains consistent.

While volatility remains a defining feature of PSIX, disciplined risk management and adherence to key support levels significantly improve the risk-reward profile across time horizons.

Conclusion & Recommendation

PSIX represents a high-growth but high-uncertainty investment opportunity BUT:

Investors should also eye:

Q4 FY2025 results validating guidance

Evidence of margin stabilization and cash-flow alignment

Resolution or dismissal of securities investigations and demonstrable improvements in governance and disclosure practices

Until this, PSIX limits margin of safety, despite its attractive headline growth and discounted valuation.

Disclaimer

This research is intended solely for educational purposes and should not be interpreted as investment advice. Readers are encouraged to conduct their own due diligence and/or consult a licensed financial advisor before making any investment decisions. All information and data presented are sourced from publicly available company filings, analyst reports, and third-party sources believed to be reliable. While this report has been prepared independently, the views expressed are personal and may contain errors or subjective bias. The author holds no financial or personal interest in the company discussed and does not own any position at the time of writing.